Never before has the phrase “chip supply chain” or “semiconductor supply chain” been such an attention-grabbing topic as today. Not only 3 million lives but also economic losses of trillions dollars have been deprived as a result of the Covid-19 pandemic, however, this event also gave us an opportunity to realize how fragile the global chip supply chain really is.

Despite the high resistance of chip, the global chip supply chain is extremely “fragile”

Although the chip itself is highly resilient to extreme temperature conditions, vibrations and external shocks, the global semiconductor supply chain appears highly vulnerable to natural disasters or unstable political situations.

When the first wave of Covid-19 swept over the world in early months of 2020, large automotive manufacturers such as General Motors, Ford Motor or Volkswagen were forced to temporarily shut down. As forecasting the continually complicated pandemic and severe decline in car demand, carmakers cancelled a series of chip orders.

Responding to this situation, chip manufacturers such as TSMC or UMC shifted their entire production capacity to produce chips for phones and laptops in the context of rapidly increasing demand for these products.

Due to a sudden surge in global car demand in the third quarter of 2020, car manufacturers struggled to ramp up production capacity, while chip producers were unable to respond quickly. Hence, the chip shortage is rapidly spreading from the automotive industry to other technology industries..

The scarcity of semiconductors has been worsened by a fire at a Japanese chip – manufacturing factory, snowstorms that caused wide and extensive power outages in the US state of Texas, and severe drought in Taiwan (China), which leads to the instant shut-down of some car production lines in the US and Europe.

This is not the first time that the chip supply chain suffered from the shortage. In fact, there was a chip shortage 10 years ago when the Fukushima earthquake damaged fabs of Renesas Electronics – a supplier of car chips. Additionally, an unusual phenomenon in the summer of 1997, when Japan’s Tamagotchi digital pet became a smash hit amongst young people around the world, the abrupt growth in demand for this product put pressure on the semiconductor manufacturer in Taiwan, hence chip shortages spread to other industries afterward.

The chip supply chain scattered but centralized

Like other industries, the chip-manufacturing industry initially followed the centralized manufacturing strategy, in which all processes took place in one country. But things started to change in 1961, when Fairchild Semiconductor, an American chip maker founded in 1957 with the headquarter in San Jose, began shifting the assembling and testing process to Hong Kong for product testing to take advantage of cheap labour costs. The disintegration trend of the chip supply chain has rapidly accelerated as chips have become more complicated and the size of this industry has become larger.

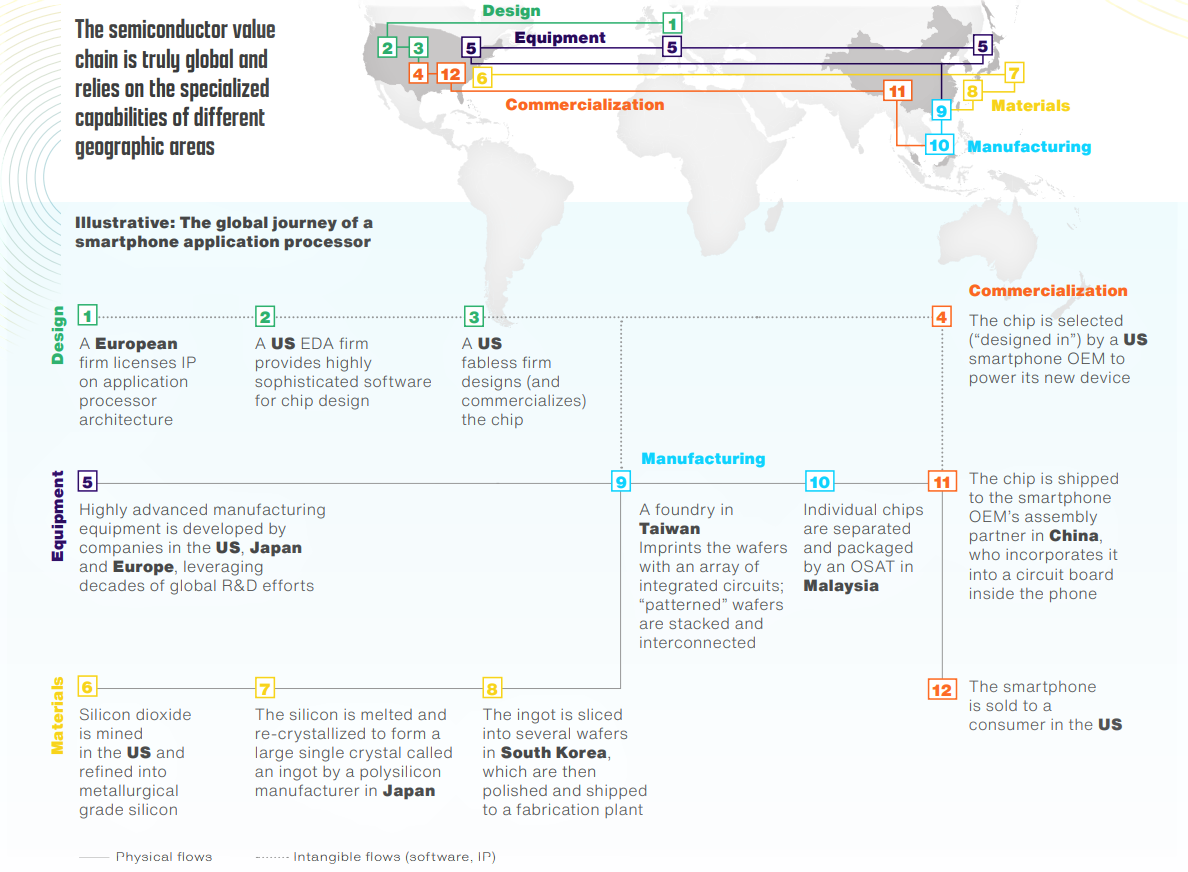

According to the latest report of BCG and Semiconductor Industry Association (SIA), more than 50 points across the entire value chain of the semiconductor manufacturing industry are recorded. In particular, a typical journey of the chip supply chain often begins in the Appalachian mountains of the US, where there are large reserves of the most high-quality silica. The mined ore, then shipped to Japan, is smelted into pure silicon ingots, and cut into wafers, the material for making microchips. Next, these wafers are moved to chip factories or fabs in Taiwan or South Korea where the patterns designed by ARM company (a British microprocessor design company) will be printed onto silicon wafers using photolithography equipment, which are mostly imported from the Netherlands.

Despite being highly fragmented, the chip supply chain is highly concentrated in some regions. China and East Asia could be described as the “Asin’s heel” of the chip supply chain, due to high risks of natural disasters and political instability there.

Specifically, in the current chip – manufacturing value chain, 75% of semiconductor production capacity is now concentrated in China and East Asia. Especially, 100% of the most advanced semiconductor production capacity (under 10 nanometers) is produced in Taiwan (92%) and South Korea (8%), these kinds of chips play an important role in the economy, national security and critical infrastructure of the United States. A study has shown that if Taiwan stops producing chips for a year, the global electronics industry will suffer from losing more than 500 billion USD in revenue or even the global electronics supply chain may be blocked.

This also explains why net chip exports from the US, Europe and Japan have decreased from 50% to less than 20% in the period from 2010 to 2020. Meanwhile, chip exports from Taiwan, South Korea, China and other Asian economies, excluding Japan, grew from 50% to more than 80% within 20 years, as of 2019.

Is it possible to restructure the chip supply chain?

To limit dependence on China, the administration of Joe Biden issued an executive order on February 24 in order to promote efforts to cooperate with allies in the field of semiconductor chips and products that play an important role in the US’s strategy. This executive order expressed the determination of the US to remove China from the chip supply chain.

However, with the supply chain structure of the semiconductor – manufacturing industry, it is impossible to separate China from the game due to Chinese factories’ large production capacity as well as the high dependence of the US on China’s rare earths supply.

It is known that the Chinese government has also directly funded domestic chipmakers about 100 billion USD. With this strong support, China sets a target to lead the world’s output of electrical cabinets with 24% market share by 2030.

While the 5G war has not yet ended, the war on chip production has become a matter of concern for many nations these days due to its importance in the economy and national security. Nevertheless, the restructuring of the chip supply chain is not “an overnight story”, lots of time and effort is required. And whether the “chip supply chain without China” is reality or imaginative is still a big question.

Huyen Tran